Financial history shows that spreadsheet errors can have staggering consequences.

Misplaced formulas have caused Fannie Mae to miscalculate a billion-dollar portfolio adjustment.

Incorrect data inputs resulted in Fidelity’s Magellan Fund misestimating dividend payouts by billions.

Cut-and-paste mistakes led TransAlta to lose $24 million.

Another costly mistake happened in 2005 when a major United States manufacturer suffered an $11 million severance error due to a typo in a spreadsheet.

Even routine processes have suffered, with companies accidentally overshooting budgets by millions after referencing the wrong file.

Yet Excel remains central in FI credit risk limit management, often extending beyond analysis into decision-making and limit governance.

That dependency introduces a structural weakness. Decisions rely on tools lacking traceability, enforceability, and consistent oversight across teams and systems.

This article examines how spreadsheet-driven limit management weakens FI credit risk control, how these gaps surface in audits and regulatory reviews, and how a modern control framework addresses them.

Spreadsheets rarely enter a bank’s architecture as a control mechanism. They emerge gradually, filling gaps between systems, processes, and reporting needs.

Over time, what begins as a support tool becomes embedded in limit governance.

FI credit risk management often relies on Excel to consolidate exposures across products such as trade finance, money markets, FX, and securities. These files evolve into internal reference points for limit monitoring, headroom calculations, and decision support.

Control, however, remains implicit rather than defined.

Limit structures, overrides, and adjustments are maintained within files that sit outside formal system boundaries. Changes depend on individual handling rather than controlled workflows. Knowledge of how limits are aggregated, adjusted, or interpreted is concentrated in a small number of users.

That creates a structural dependency.

Limit governance operates through tools that were never designed to enforce policy, maintain audit trails, or ensure consistency across systems.

The spreadsheet becomes a silent control layer, influencing exposure decisions without being formally recognised as one.

Visibility suffers as a result.

Different teams may rely on different versions of the same file, each reflecting a slightly different view of exposure and available capacity. Alignment depends on timing, coordination, and manual reconciliation rather than system-driven consistency.

Decisions are made based on outputs that cannot be fully traced, validated, or enforced across the transaction lifecycle. What appears stable on the surface depends on fragile structures underneath.

In FI credit risk management, that fragility directly affects how limits are interpreted, applied, and governed across the institution.

A recent survey found that 42 % of financial institutions and 70% of compliance teams still rely on manual processes “often” for compliance tasks, despite growing regulatory complexity.

Spreadsheets may appear reliable, but their role as an informal control layer conceals structural weaknesses.

Limit oversight, approvals, and adjustments often rely on manual handling, scattered files, and implicit knowledge.

The following sections examine how these vulnerabilities undermine control, reduce accountability, and create gaps that only surface under audit or stress.

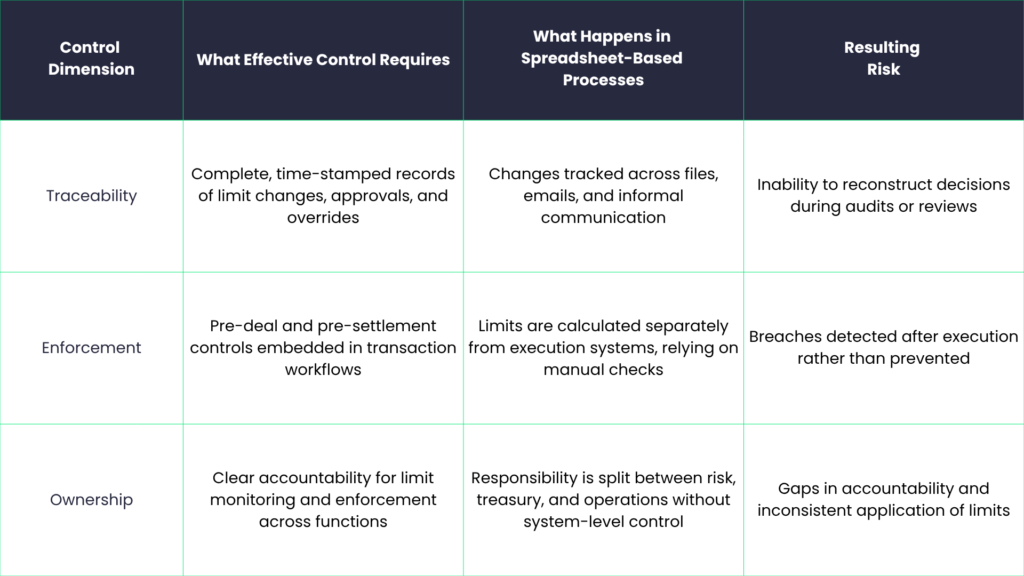

Effective FI credit risk control relies on three core elements: traceability, enforcement, and clear ownership.

Spreadsheet-driven processes weaken each of them in ways that remain largely invisible until a breach or audit brings them into focus.

Operational spreadsheets can contain errors in more than 1 % of their formula cells, even without obvious failures, meaning hidden inaccuracies accumulate as files scale and link across teams.

These gaps are structural rather than operational.

These weaknesses do not operate independently.

Limited traceability reduces accountability.

Lack of enforcement increases reliance on manual intervention.

Diffused ownership creates uncertainty around which figures reflect actual exposure.

The process continues to function, but without the characteristics required for consistent, defensible control.

Control gaps rarely surface during normal operations. They become visible when decisions need to be explained, validated, and reproduced under scrutiny.

Audit and regulatory reviews focus on a simple expectation: decisions must be traceable from approval to execution, with clear evidence at every step. Spreadsheet-driven environments struggle to meet that standard.

Limit changes, overrides, and approvals exist, but the evidence remains scattered.

Version histories, email threads, and manually updated files must be reconciled to rebuild a single decision path. That reconstruction introduces delays, inconsistencies, and dependency on individual input.

Auditors increasingly raise concerns that spreadsheet data can be modified, deleted, or manipulated without oversight, making it difficult to rely on spreadsheets as evidence for financial reporting or credit decisions.

Reproducibility becomes the central issue.

Decisions on limits from previous days or weeks cannot be reliably reproduced. Different file versions, timing of updates, or manual adjustments outside formal workflows can yield varying exposure figures.

That creates a gap between decision and proof.

From a risk perspective, the limit may have been respected. From an audit perspective, the institution cannot demonstrate it with certainty. This distinction carries weight in supervisory reviews, where evidence holds more value than intent.

The pressure increases in stress scenarios.

During volatility, exposures shift rapidly, limits are adjusted more frequently, and exceptions become more common. The ability to demonstrate how decisions were made, and whether they aligned with policy at that exact point in time, becomes critical.

Without a controlled system of record, that level of clarity is difficult to achieve.

In FI credit risk management, auditability is part of the control framework itself. When decisions cannot be reproduced cleanly, the framework loses credibility, regardless of the outcome.

Spreadsheets cannot enforce limits, track approvals consistently, or prevent breaches in real time.

Globit replaces these fragile manual workflows with a structured control layer embedded directly in transaction processes.

Real-Time Limit Enforcement: Transactions are automatically checked against approved limits at booking or settlement, preventing exposures from exceeding risk appetite.

Single Source of Truth: All counterparty limits and exposures are centralised, ensuring consistent data across risk, treasury, and operations teams.

Automated Audit Trails: Every override, adjustment, and approval is logged, making decisions fully traceable and defensible for audits and regulatory review.

Scalable Architecture: Adding new counterparties, products, or limits does not increase operational risk; controls scale with the portfolio.

By moving from reactive, spreadsheet-based processes to an always-on, enforceable system, institutions reduce errors, improve compliance, and make limit management auditable and reliable.

Every bank will eventually exist in a spreadsheet-centric FI limit management. The only question is whether you choose the moment, or the moment chooses you.

You can wait for the next volatility spike, when exposures move, and your numbers don’t. You can wait for the next regulator visit, when “last saved” becomes your best evidence. You can wait for a key person to leave and take the macros with them.

Or you can move first. Treat Excel as what it is now: useful for analysis, unacceptable as a control layer. Put an API-first limit engine in the transaction flow, where limits actually matter. Give your board and regulators a traceable, defensible story, backed by logs, approvals, and real-time enforcement.

This isn’t about working faster in Excel; it’s about outgrowing it.

Stop managing limits. Start orchestrating risk. Discover Globit’s High-Performance FI Solutions!